Artificial Intelligence

April 18, 2024

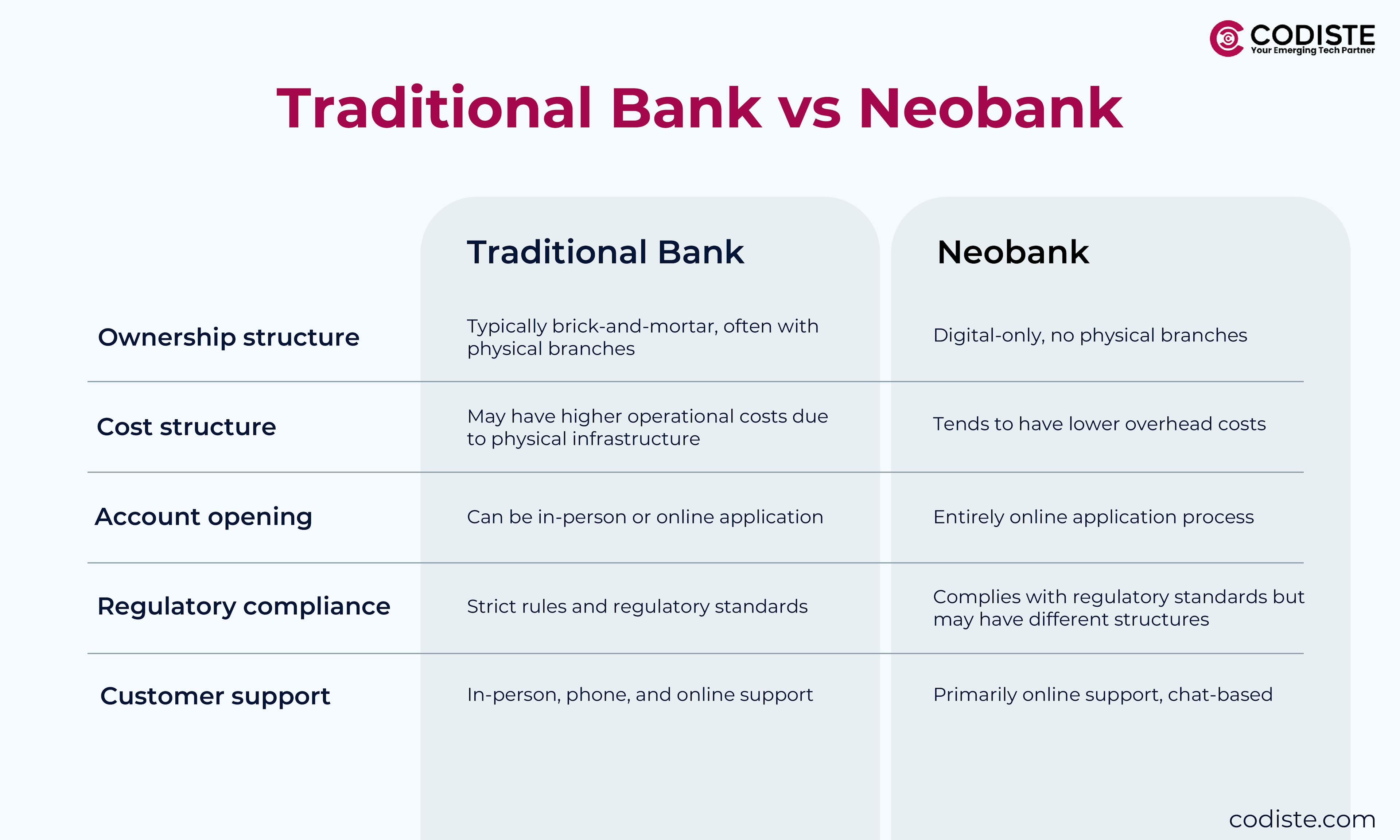

The fight between neobanks vs traditional banks isn't simply about online banking vs physical offices anymore. It's about alternative ways of thinking about banking technology innovation that are changing how banks work, compete, and help clients in 2025.

By 2025, there were around 394 million neobanking users globally. For traditional banks, 77% of checking account holders were active digital banking users in 2025. This confluence shows that the race for invention has moved past the classic story of David vs. Goliath and into something much more complex.

The question here isn't whether neobanks will take the place of traditional banks. Instead, it's about which new ideas will shape the future of financial services and what that implies for entrepreneurs, strategists, and investors who want to get ahead in this fast-changing field.

Digital transformation in banking has given neobanks unique competitive advantages that they use as fundamental differentiators instead of extra features. Their architecture-first strategy lets them do things that older banks have a hard time doing with their old systems.

There is a big difference in timing. Neobanks can add new features in weeks, but traditional banks need months or quarters. It's not only about being agile; it's also about making innovation a part of the foundation instead of adding it on top.

Neobanks benefit from lower cost structures, often a fraction of what traditional banks incur, due to minimal physical infrastructure and automation-heavy back ends. This operational efficiency translates directly into innovation velocity that traditional banks find difficult to match.

Legacy financial institutions aren't sitting idle while neobanks capture market share. Digital transformation in banking has accelerated dramatically, with traditional banks investing billions in technology modernization and AI in banking capabilities.

The surprise development in 2025 is how effectively some traditional banks have adapted neobank strategies while maintaining their regulatory advantages and customer trust foundations.

Traditional financial institutions are acting more like neobanks as regulators draw a bead on neobanks, creating competitive dynamics where legacy players adopt challenger strategies while neobanks face increasing regulatory scrutiny.

Customer experience in banking has become the primary battleground where neobanks vs traditional banks competition plays out most visibly. The difference lies not just in interface design, but in fundamental service philosophy and operational approach.

Neobanks built their entire value proposition around friction elimination. Every process, from account opening to transaction processing, prioritizes speed and simplicity over comprehensive service options.

Traditional banks initially struggled to match this experience quality, but the gap is narrowing rapidly. Big banks now have digital onboarding processes and mobile-first interfaces that are just as good as those at neobanks.

The major difference is still how they prioritize things. Neobanks make every encounter as efficient as possible for digital use, while traditional banks balance digital experience with a wide range of services and the need to follow rules.

AI in banking represents the most significant differentiator in the neobanks vs traditional banks innovation race. The approaches, capabilities, and implementation strategies reveal fundamental differences in how these institutions view technology's role.

Neobanks view AI as fundamental infrastructure that is included in all operational procedures and consumer interactions. Within their current operating frameworks, traditional banks selectively apply AI, concentrating on particular use cases.

Neobank AI integration:

Traditional bank AI adoption:

Banks need to move beyond experimentation to transform critical areas, including by reimagining complex workflows with multi-agent systems, indicating that traditional institutions recognize the need for more comprehensive AI integration strategies.

Ready to navigate the evolving banking innovation landscape?

Banking regulation creates a complex innovation environment where neobanks vs traditional banks face different advantages and constraints. This regulatory landscape is shifting rapidly as authorities adapt oversight frameworks to digital-first financial services.

Traditional banks operate with established regulatory relationships and proven compliance systems. Neobanks benefit from newer regulatory frameworks designed for digital financial services, but face increasing scrutiny as they scale.

Traditional bank regulatory advantages:

Neobank regulatory positioning:

The regulatory climate is becoming favorable for institutions that can show both innovative capabilities and operational stability. This balancing poses problems for both neobanks and traditional banks in different ways.

The neobanks vs traditional banks performance metrics reveal a more complex picture than simple growth comparisons suggest. Success depends heavily on how you define winning in the current financial services landscape.

Neobanks excel in user acquisition speed and engagement metrics. Traditional banks dominate in profitability, asset management, and comprehensive service delivery. The market is rewarding different strategies in different segments.

Neobank strengths:

Traditional bank advantages:

The most successful institutions in 2025 are those combining neobank innovation velocity with traditional bank operational stability and regulatory expertise.

Banking platform strategies are emerging as the winning approach, where traditional banks and neobanks increasingly collaborate rather than compete directly. This convergence creates new opportunities for innovation while addressing respective limitations.

Neobanks can use Banking-as-a-Service models to offer their digital experience and innovation skills while leveraging the capital and regulatory licenses of traditional banks. Without having to overhaul their fundamental systems, traditional banks can use neobank technology and client acquisition tactics.

How neobanks are different from traditional banks is becoming less about how they organize their operations and more about their strategic emphasis, how they group their customers, and their priorities for new ideas.

The neobanks vs. traditional banks environment gives you a lot of strategic choices based on where you are in the market, who your clients are, and what your competitive aims are. The decision between neo-banks vs traditional banks is changing into portfolio strategies that use both types of banking.

The decision matrix for fintech founders now includes partnership opportunities with traditional banks alongside direct competition. For traditional institutions, the question shifts from whether to digitize to how quickly digital transformation can be implemented without compromising operational stability.

The strategy is now more about understanding where neobank innovations create genuine value versus where traditional banking capabilities remain essential. Customer experience in banking needs both digital sophistication and operational stability, which makes hybrid methods better than pure-play alternatives.

Codiste, with its extensive knowledge, combines deep banking domain expertise with a taste for digital innovation capabilities, helping organizations build solutions that leverage the best of both traditional banking and neobanking. Whether you're evaluating partnership opportunities, competitive strategies, or investment decisions, the current dynamic requires a specialized understanding of both digital transformation and financial services operations, and Codiste is your best bet for it. Consult with our experts now.

Every great partnership begins with a conversation. Whether you're exploring possibilities or ready to scale, our team of specialists will help you navigate the journey.